Download the notebook here!

Interactive online version: ![]()

Hyperbolic discounting

Time preference parameters in structural models of dynamic discrete choices are underidentified, which is especially problematic for counterfactual analysis, since information on time preferences are needed to make any statement about the behavioral response of the agents to a policy intervention.

In the literature, both theoretical arguments for identification and empirical identification strategies exploit variables that leave the per-period utility function unaffected, while being relevant to the agents’ decisions. The intuition is that comparing the behavioral response of similar agents to different (expected) futures may reveal information on their time preferences.

Here we explore the practical identification of the time preference parameters in a discrete choice dynamic model of occupational choice with (quasi-)hyperbolic discounting and naïve agents, after introducing empirically-motivated exclusion restrictions that influence the size of the agents’ choice set.

[1]:

import yaml

import pickle

import pandas as pd

import respy as rp

from auxiliary import compare_choice_probabilities

from auxiliary import plot_heatmap3d

from auxiliary import plot_counterfactual_predictions

import seaborn as sns

sns.set_context("notebook", font_scale=1.5)

sns.set_style("white")

Motivation

Exponential and hyperbolic discounting

The class of discrete choice dynamic programming (DCDP) models has been used to explore the potential effect of policy changes in a host of different domains. Indeed, a unique payoff of structural econometric models is the possibility to simulate model outcomes in counterfactual environments, thus generating predictions useful to answer what-if questions that may be relevant for policy-making purposes.

The vast majority of DCDP models assume the agents to be endowed with exponential time preferences, such that their intertemporal utility can be represented by the sum of instantaneous utilities weighted by a discount factor, usually denoted by \(\delta\), which is constant across periods:

Introduced by Samuelson (1937), exponential discounting is routinely taken as an assumption in problems of intertemporal choice, but its realism has been questioned starting from Samuelson himself, who made no claims about the normative nor the descriptive validity of the functional form he was proposing. In fact, there exist a large literature providing evidence that people discount time in an hyperbolic rather than exponential fashion: That is, they discount time more heavily over shorter horizons than over longer horizons (“present bias”).

Multiple functional forms have been proposed to account for hyperbolic discounting. A formulation which is widely used, mostly for its tractability, is the \(\beta - \delta\) model (Phelps and Pollak, 1968):

This formulation implies a declining discount rate between period t and period t + 1, determined by both \(\beta\) and \(\delta\), which should be respectively interpreted as a parameter capturing present bias and the long-run discount factor. However, the discount rate between any two future periods is constant, and determined solely by \(\delta\). Exponential discounting is therefore nested within the \(\beta - \delta\) model for \(\beta\) equal to 1.

Additionally, agents can be more less sophisticated with respect to their time preferences. A sophisticated agent correctly perceives, at each point in time, his next period self to have a present bias parameter \(\beta\). A partially naïve agent underestimates his future selves’ present bias, while in the extreme case a completely naïve agent believes his future selves to have \(\beta = 1\) (i.e. to be exponential discounters).

Time preferences in DCDP models

The last decade has seen a growing interest in integrating models of hyperbolic discounting within the DCDP framework. Many of these attempts have been concerned with assessing the relevance of behavioral responses due to present biased preferences, typically benchmarked against the exponential discounting model, for the evaluation of social policies. However, testing the exponential versus the hyperbolic model can be problematic, as the actions of exponential and hyperbolic discounters can be observationally equivalent.

Theoretical results on identification with quasi-hyperbolic discounting formalize the intuition that time preferences can be recovered comparing the behavior of agents that only differ in their “futures”, where future in this context usually refers to the evolution of the state space. If agents are otherwise identical, differences in their behavior are solely determined by how they discount the utility stream from future periods.

Here we study the identification of time preference parameters in a model of occupational choice where agents can face exogenous restrictions on their employment possibilities. Such restrictions should aid identification, because they do not affect the per-period utility function but matter for choice: Future-oriented agents take the restrictions into account when deciding on their level of education.

Model

The basic set-up follows Keand and Wolpin (1994). In each period \(t\), identical agents choose among four mutually exclusive alternatives: Work in either occupation A or occupation B, continue education, or remain at home. The departures from this model are the following:

Agents are completely naïve (quasi-)hyperbolic discounters. Their time preferences are described by the discount factor \(\delta\) and the present bias \(\beta\).

Agents may face a restricted choice set, depending on the exogeneous “restriction regime” they face.

Unrestricted agents can choose any alternative in any period,

Restricted agents need at least 12 years of education to choose occupation B,

Very restricted agents need at least 12 and 14 years of education to choose occupation A or occupation B, respectively.

Therefore, while the assignment to the restriction regime is exogeneous, whether the agent actually experience employment restrictions depends deterministically on their educational choices.

Identification strategy

Experiencing a restriction on one or more occupational choices does not enter the instantaneous utility function from choosing to stay in school, but it raises the option value of education and therefore its expected discounted stream of utility. The degree to which agents adjust their educational decision should be informative of their time preferences.

*Notes*: Effect on the choice set of a choice restriction, if the agent has 13 period of experience in education in t. For simplicity, the home alternative is removed. Choosing the education alternative in any period t + n allows the agent to choose occupation B starting from period t + n + 1. An unrestricted agent can choose any alternative in any period.

Simulating the data

The “observed” data are two datasets with 10,000 agents observed for 40 periods.

[2]:

# load params

params = pd.read_csv("specs/params_hyp.csv", sep=";", index_col=["category", "name"])

params["value"] = params["value"].astype(float)

# load options

with open("specs/options_hyp.yaml") as options:

options = yaml.safe_load(options)

# change seeds to simulated "observed" data

options["solution_seed"] = 0

options["simulation_seed"] = 1000

[3]:

simulate = rp.get_simulate_func(params, options)

df = simulate(params)

Visualizing the data

[4]:

fig = compare_choice_probabilities(df=df)

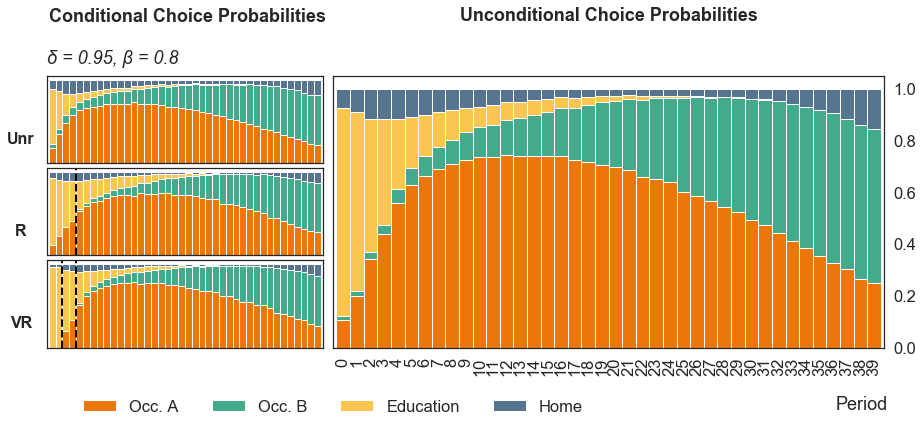

*Notes*: Model of occupational choice based on Keane and Wolpin (1994), one dataset with 1,000 simulated agents and 40 observed periods. The figure shows choice probabilities conditional for unrestricted agents (**Unr*), restricted agents who face one restroction on occupation B (R) and very restricted agents who face one restriction on A and one on B (VR). In R, the dashed line indicates the first period in which agents can potentially choose occupation B, as the initial conditions of the model ensures that all agents start with 10 years of education. In VR, the dashed lines indicate the first period in which agents can potentially choose occupation A and occupation B, after 12 and 14 years of education respectively.*

At the beginning of the life-cycle the choice is among education, home, and occupation A, since occupation B provides large returns only when agents have accumulated experience in education and/or occupation A. The utility from education is low, and it becomes negative if agents go to college. Hyperbolic discounters choose the home alternative more often than exponential discounters: A lower present bias makes education less attractive, as future gains are discounted more heavily.

Agents who face one or two restrictions tend to stay in education longer than those who don’t, as choice restrictions increase the option value of education:

The exponential discounters who face restrictions stay longer in education and delay their entrance in the job market, while the share of agents shifting to the home alternative (which mostly happens at the end of the life-cycle) is nearly unchanged.

The hyperbolic discounters who face restrictions similarly delay their entry in the job market. However, the share of those who choose the home alternative in the initial periods decreases. This is consistent with the intuition that hyperbolic discounter are more sensitive to educational incentives, because they stay in education shorter than optimal in the first place.

Practical identification

In practice, whether the time preference parameter(s) can be identified from the data depends on the curvature of the criterion function. Consider the problem of estimating a model with exponential discounting on observational data: If the criterion is computed as a function of \(\delta\) only, while all the other parameters are set a their respective estimates, we need the criterion to exhibit a unique minimum (or maximum) between 0 and 1 to recover \(\delta\).

In this exercise, the Method of Simulated Moments (McFadden, 1989) criterion function is computed as a function of \(\beta\) and \(\delta\) only, making the optimization problem two-dimensional. The other parameters are set at their true, rather than estimated, values. This overcomes the hurdles of the real estimation process, simplifies the exposition and aids the visualization of the results. However, it represents a “best case scenario” where practical identification is not complicated by inaccurate estimates of the other model parameters.

The moments used for estimation are per-period choice probabilities, conditional on restriction regime, and the per-period wage profile (mean and standard deviation) of those who work, again conditional on restriction regime. The weighting matrix is a diagonal matrix where the weights are the inverse variances of the observed sample moments, computed via a bootstrapping procedure.

[5]:

df_heatmap = pd.read_csv("data/heatmap.csv")

[6]:

fig = plot_heatmap3d(df_heatmap)

*Notes*: Evaluations of Method of Simulated Moment’s criterion function for model with hyperbolic discounting based on Keane and Wolpin (1994), for different value of discount factor and present bias. The candidate structural model with hyperbolic discounting coincides with the true data-generating process of the “observed” dataset. However, the empirical moments do not perfectly coincide with the simulated moments because of random variation in the payoff shocks, which induces variation in the agents’ choice probabilities. This implies that the criterion function is not necessarily minimized at the true parameter vector for a given finite sample.

In the figure above, the darker the area, the lower the value of the criterion function associated with the corresponding combination of \(\beta\) and \(\delta\).

A global minimum exists, but there is no basin around it. Instead, the criterion function takes similar values for combinations of the time preference parameters where \(\beta\) is underestimated with respect to the true value and \(\delta\) is overestimated, and vice versa. This pattern is similar to the “banana-shaped through” found in Abbring et al. (2018) and Laibson et al. (2007), which consider models that are different from the one presented here.

When \(\beta\) is fixed at 1 (corner case of exponential discounting), the criterion function attains the lowest value for a value of the discount factor which lower than the true one. This is consistent with the intuition that a misspecified exponential model fitted on hyperbolic dataset needs a lower discount factor to rationalize the data.

Counterfactual predictions

The heatmap above points at the practical difficulty of disentangling the time preference parameters in estimation. A relevant question is then whether different combinations of the two parameters produce similar counterfactuals.

The figure below represents the effect of a 2000 USD tuition subsidy on the experience in education accumulated over the life-cycle, as predicted by the true model and two misspecified models.

[7]:

with open("data/subsidy_effect.pickle", "rb") as input_file:

subsidy_effect = pickle.load(input_file)

[8]:

data = {

"true": subsidy_effect["true"],

"exponential": subsidy_effect["exp"],

"global_min": subsidy_effect["global_min"],

}

[9]:

fig = plot_counterfactual_predictions(data, "Experience_Edu", "Years of Education")

*Notes*: Effect of tuition subsidy of 2000 USD on average years of education in each period, predicted by true model and misspecified models. The average is computed over 100 datasets with sampling variation, each with 10,000 agents observed for 40 periods. The shaded areas visually represent the simulation error.

Bibliography

Abbring, J. H., Daljord, Ø., & Ishakov, F. (2018). Identifying present-biased discount functions in dynamic discrete choice models.

Keane, M. P., & Wolpin, K. I. (1994). The solution and estimation of discrete choice dynamic programming models by simulation and interpolation: Monte carlo evidence. The Review of Economics and Statistics, 76(4), 648–672. https://doi.org/10.2307/2109768

Laibson, D. I., Repetto, A.,&Tobacman, J. (2007). Estimating discount functions with consumption choices over the lifecycle (Working Paper No. 13314). National Bureau of Economic Research. https://doi.org/10.3386/w13314

McFadden, D. (1989). A method of simulated moments for estimation of discrete response models without numerical integration. Econometrica, 57(5), 995–1026. http://www.jstor.org/stable/1913621

Phelps, E., and Pollak, R. A. (1968). On second-best national saving and game-equilibrium growth. The Review of Economic Studies, 35(2), 185–199. https://doi.org/10.2307/2296547

Samuelson, P. A. (1937). A note on measurement of utility. The Review of Economic Studies, 4(2), 155–161. https://doi.org/10.2307/2967612